Highlights of the report:

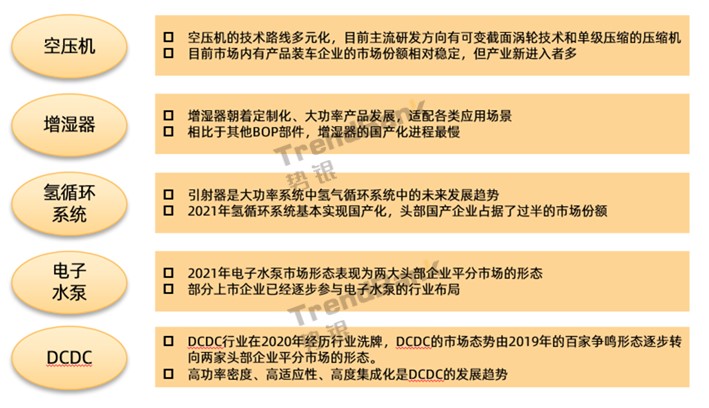

• The air compressor industry is still in the early stage of industrial development, and the market concentration is high

• The two technical routes of the hydrogen cycle system are parallel, and themarket concentration is reduced

• The degree of localization of humidifiers has steadily increased, and themarket concentration has decreased

• DCDC has experienced industry reshuffle, with high market concentration

• There are few players in the electronic water pump market, and the market concentration is high

• Foreign brands are deploying important components in the BOP field

• In the future, companies with fuel cell system BOP with iterativecost reduction technology will have certainadvantages in the market

At present, in each component of the BOP industry chain of the fuel cellsystem, the market situation of each component industry is different. Forexample, the air compressor industry is still in the early stage of industrial development, and the market concentration is high, while the two technical routes of the hydrogen cycle system are parallel. Concentration drops.

From the perspective of localization, the hydrogen circulation system, air compressor and DCDC are basically localized atpresent, and the in-rolling market has led to extremely fierce competition.Among them, the DCDC has certain requirements on the R&D capabilities ofenterprises due to the rapid change in the power of the fuel cell system. Around of shuffling has been completed; humidifiers are relatively low inlocalization, and the market is currently showing a trend of accelerating domestic substitution. In addition, compared with other BOP industries, thereare few players in the electronic water pump market, and the market concentrationis high.

The air compressor industry is still in the early stage of industrial development, and the market concentration is high

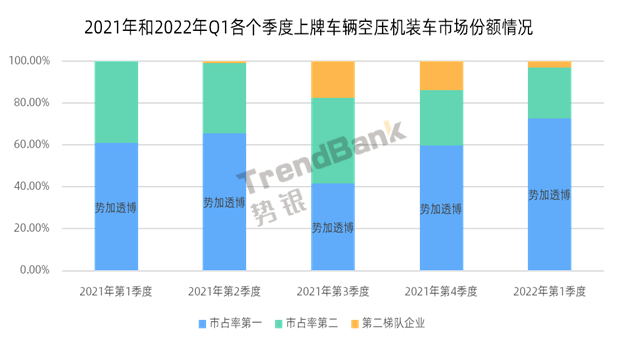

In 2021 and 2022Q1, in terms of the market share of air compressors onlicensed vehicles, TOP2 companies currently occupy most of the market share,and this situation has lasted for a year, indicating that TOP2 companiesal ready have strong market competitiveness.

Although the second-tier companies in the third quarter of 2021 and the fourth quarter of 2021 have a certain amount of product loading, the top 2 companies in the first quarter of 2022 have regained more than 97% of the market share, so It is speculated from Trendbank that the market share of air compressors will hardly change significantly in the short term.

Source: TrendBank

The number of companies in the air compressor field is increasing, and the market competition is intensifying

According to the Trend bank database, the air compressor market in 2019 wasmainly occupied by foreign companies. The company with the highest market sharewas Garrett, and the TOP4 companies were all foreign brands. However, somedomestic companies also occupied a small part of the market share.

By 2021, the TOP4 companies have completed domestic substitution, together accounting for about 95% of the market share. From the perspective of market form, in 2021, there are only 7 air compressor companies with fuel cellsinstalled on vehicles, and only 4 air compressor companies with shipments exceeding 100 sets. As a leading company, XecaTurbo has occupied nearly 60% ofthe market share. it can be seen that the fuel cell air compressor industry isstill in the early stage of industrial development.

Source: TrendBank

Under the background that the air compressor industry is in the earlystage of industrial development, many traditional air compressor companies and related capital continue to enter. For example, Wenli Technology, Birkenstock Energy Saving, China Entropy New Energy, and Huajian New Energy have also successively released highly competitive air compressor products in recentyears. And foreign brands such as Bosch and Spenders are also gradually grabbing market share. It is still unknown that the entire market competition pattern will under go dramatic changes in the second half of 2022. The figure below is an over view of the current air compressor companies in the industry.

Source: TrendBank

The two technical routes of the hydrogen cycle system are parallel, and the marketconcentration is declining

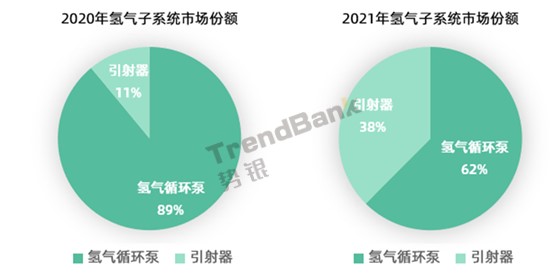

Compared with 2020, the market share of ejectorsin hydrogen subsystems will increase from 11% to 38% in 2021. There are two main reasons. Firstly, ejector companies have solved technical problems and achieved full power coverage. Secondly, some system companies have completed the testing and verification of ejector technology and have begun to apply them to the market. Trendbank predicts that in the next 1 to 2 years, the technical route of the hydrogen circulation system will still be dominated by hydrogen circulation pumps.

Technical level -the ejector needs to be adapted to a mature fuel cell system

At present, most fuel cell vehicles are in the market verification stage, and the products change rapidly, and parameters need to be adjusted frequently at the system level. The ejector solution needs to beadapted to a mature system. Any adjustment of system parameters will result in the ejection not reaching the optimal efficiency of the system.

Cost level - fuelcell vehicles do not achieve cost-effectiveness through scale effect.

At present, the sales of fuel cell vehicles in China are mainly driven by government policies and are not yet in the commercialization stage. The sales volume of the same type of fuel cell systemhas not exceeded 100. The difference between the comprehensive cost of the circulating pump and the ejector is difficult to offset the design cost of theejector solution, and the economy of the ejector solution is not realized through the scale effect.

Source: TrendBank

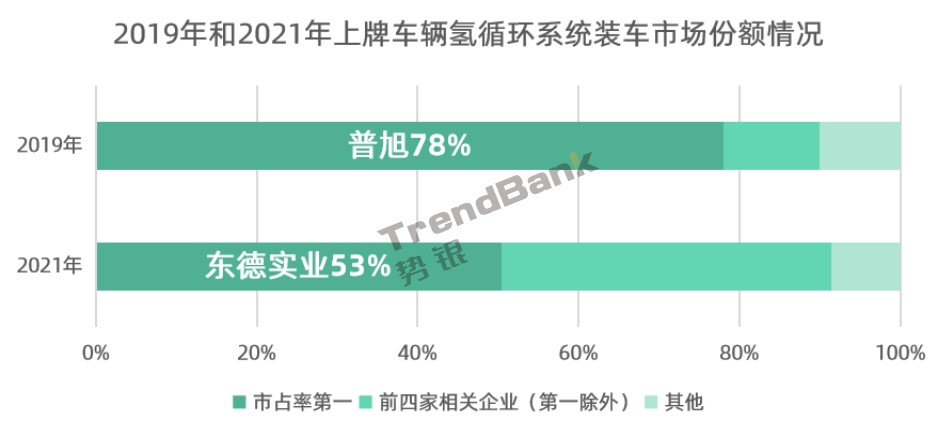

In 2019, the market share of hydrogen circulation systems was mainlyoccupied by foreign companies, and most of the solutions at that time used hydrogen circulation pumps. Among them, the company with the highest market share is Busch, and at that time Busch, as the leading company in the hydrogencycle system, occupied nearly 78% of the market share. By 2021, three of the TOP4 companies will be domestic brands, and together they will occupy nearly 92% of the market share. Among them, Dongde Industrial, as a leading company,will occupy more than 50% of the market share.

Source: TrendBank

The degree of localization of humidifiers has steadily improved, and the marketconcentration has declined

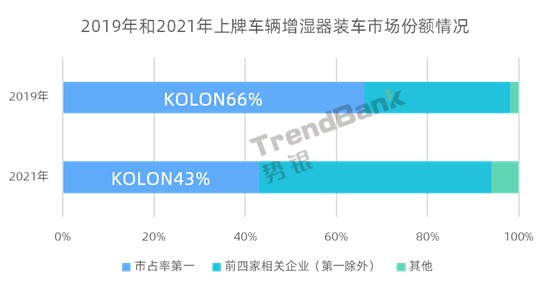

According to the TrendBank database, the market share of humidifiers in 2019 is mainly occupied by foreign companies, of which the company with the highest market share is KOLON, and the TOP4 companies areall foreign brands. In addition, in 2019, there are no domestic brandhumidifiers for fuel cell vehicles that are loaded on the licensed vehicle.

By 2021, three of the TOP4 companies will still be foreign-owned brands,but the domestic benchmark company Extender has completed the development of 0-240Kw products, and has occupied more than 30% of the market share among 2021 licensed vehicle.

Source: TrendBank

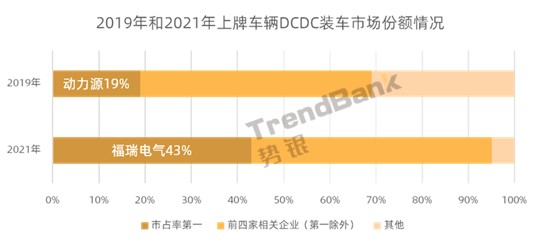

DCDC has experiencedindustry reshuffle, with high market concentration

In 2019, the domestic market of DCDC showed that a hundred schools of thought contended, with more than 10 DCDC companies eachoccupying a small market share; the refore, the market concentration was verylow. In the 2020 industry reshuffle, SHINRY and Foripower rose to the challenge and occupiedmost of the market share.

By 2021, the two leading companies, SHINRY Technologyand Foripower Electric, will occupy more than 80% of the market share. From the perspective of changes in market concentration, the market situation of DCDC has gradually shifted from the form of a hundred schools of thought contendingin 2019 to the form of two leading companies sharing the market equally.

Source: TrendBank

There are fewplayers in the electronic water pump market, and the market concentration ishigh

According to the TrendBank database, Aier is the first company to localize electronic water pumps and has a market share ofnearly 57% in 2019. By 2021, the TOP2 companies are all domestic brands, and together they occupy nearly 97% of the market share. Among them, Aier, as the leading company, occupies more than 55% of the market share, while the marketshare of Hefei Xinhu has steadily increased. In addition, Feilong Electronics,as a leading enterprise of automobile water pump, is actively deploying theelectronic water pump industry.

Source: TrendBank

Foreign brands are deploying importantcomponents in the BOP field

At present, the domestic BOP market has basicallyachieved domestic substitution. However, many foreign brands are deploying important components in the BOP field and gradually increasing the market share of their products. Therefore, the market competition in the BOP field will be further intensified in the future. The following is the product status and market situation of domestic and foreign brands in the domestic BOP market included in TrendBank.

Source: TrendBank

In the future, companies with fuel cell system BOP with iterative cost reduction technology will have certain advantages in the market

Trendbank focuseson the market situation of various components of fuel cell system BOP, keyenterprises and the technological development trend of various components. It is found that there are two important reasons why the current hydrogen fuelcell market size and market share have not been able to develop and expandrapidly. They are high cost and rapid system integration iteration. It isdifficult for components such as fuel cell components and electronic controlsystems to achieve upstream and downstream industries. Collaborative production, so it is difficult to achieve the effect of mass production and cost reduction.

The refore, Trendbank believes that companies with fuel cell system BOP with iterative cost reduction technology will have a certain advantage in the market in the future.

Source: TrendBank